Mumbai (Maharashtra) , July 21: Open an economics textbook and you’ll get a clean, reassuring story: investors crunch numbers, weigh…

Read More

Mumbai (Maharashtra) , July 21: Open an economics textbook and you’ll get a clean, reassuring story: investors crunch numbers, weigh…

Read More

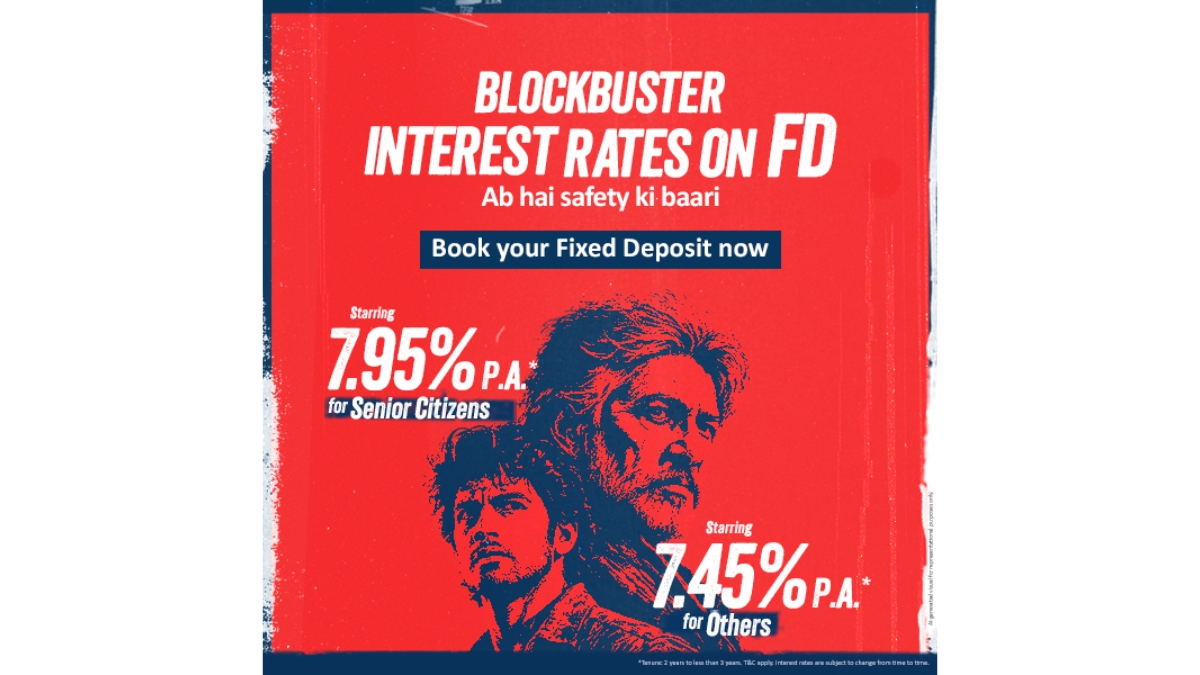

Kolkata (West Bengal) , July 14: Savers seeking stronger yet stable returns have a fresh reason to consider fixed deposits.…

Read More

New Delhi , July 11: “Budget your money.” We’ve all heard it, right? For beginners, tracking every cup of coffee…

Read More

New Delhi , July 3: Metro city living brings better access to hospitals, specialists, diagnostic centres, and advanced treatments. Still,…

Read More

Gandhinagar (Gujarat) , July 3: Photonics Watertech Limited is engaged in providing end-to-end services in (i) LED-based lighting solutions; (ii)…

Read More

New Delhi , June 30: Over 75% of new crypto activity in India now comes from Tier-2 and Tier-3 cities.…

Read More

New Delhi , June 29: Regulatory authorities and financial oversight bodies are reportedly reviewing activities related to online forex trading…

Read More

Mumbai (Maharashtra) , June 10: A critical illness benefit is not something you must add to a health plan just…

Read More

Mumbai (Maharashtra) , June 9: Health insurance in India is becoming more policyholder-focused, with greater attention on clarity, continuity, service…

Read More

Mumbai (Maharashtra) , June 4: Renewing car insurance for an older vehicle is often treated as a routine task, but…

Read More