New Delhi , May 29: When people talk about gold in India, the conversation usually stays personal. It is about…

Read More

New Delhi , May 29: When people talk about gold in India, the conversation usually stays personal. It is about…

Read More

Mumbai (Maharashtra) , May 28: A car insurance policy includes several terms and conditions that may affect the claim process…

Read More

New Delhi , May 26: India’s digital lending ecosystem is witnessing a major shift towards compliance-led growth, transparent lending practices,…

Read More

New Delhi , May 20: Inflation is one of the most underestimated threats to long‑term wealth. It rarely announces itself…

Read More

Pune (Maharashtra) , May 20: MBank, The Muslim Cooperative Bank Ltd., Pune, one of Maharashtra’s most trusted urban cooperative bank,…

Read More

Pune (Maharashtra) , May 19: Bajaj General Insurance Limited (formerly known as Bajaj Allianz General Insurance Company Limited), one of…

Read More

Mumbai (Maharashtra) , May 19: Electric two-wheelers are appearing in more neighbourhoods and on more routes, from short office commutes…

Read More

Anuj Agrawal, Founder & CEO Of Zyon Group Bengaluru (Karnataka) , May 12: Bengaluru has been under siege—not from competition,…

Read More

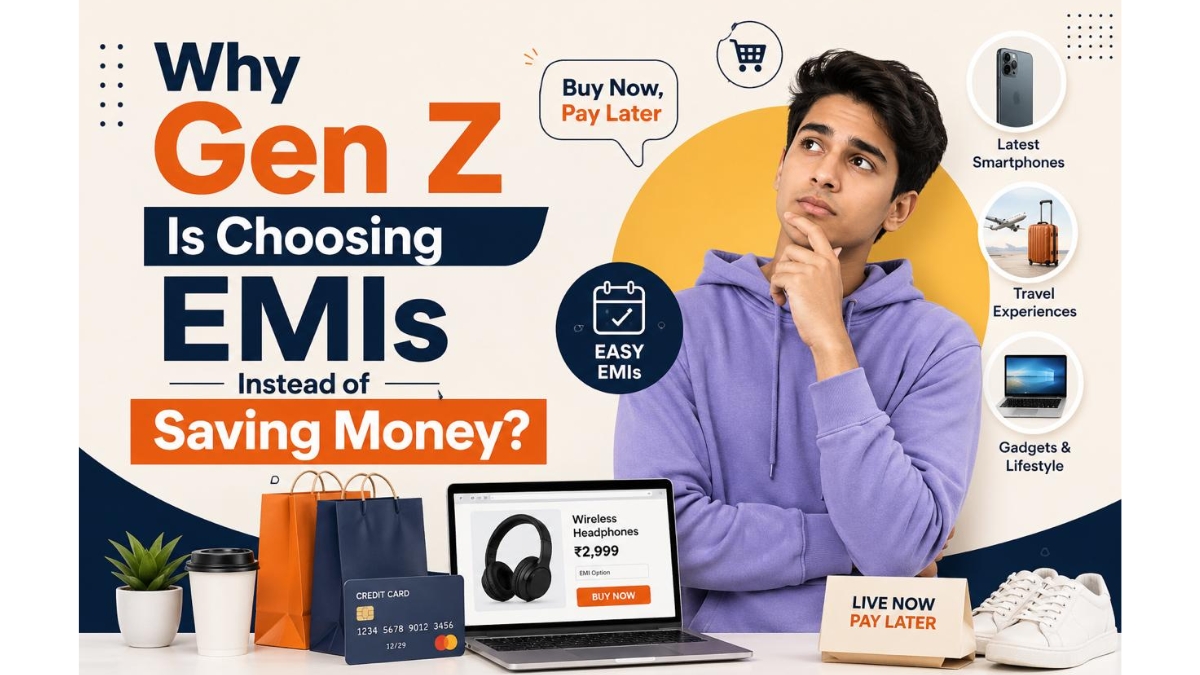

The Shift from Saving to Spending New Delhi , April 30: Financial wisdom in India had been based on one…

Read More

New Delhi , April 29: In a trading world often clouded by skepticism, few names have managed to build genuine…

Read More